No Credit vs Bad Credit: What the Difference Means for You

What does no credit mean?

No credit means you have no borrowing history on file with the three major credit bureaus: TransUnion, Equifax, and Experian. If you have never opened a credit card, taken out a loan, or financed a purchase, your credit report is essentially empty. The Consumer Financial Protection Bureau estimates that roughly 26 million Americans are “credit invisible,” meaning they have no credit file at all.

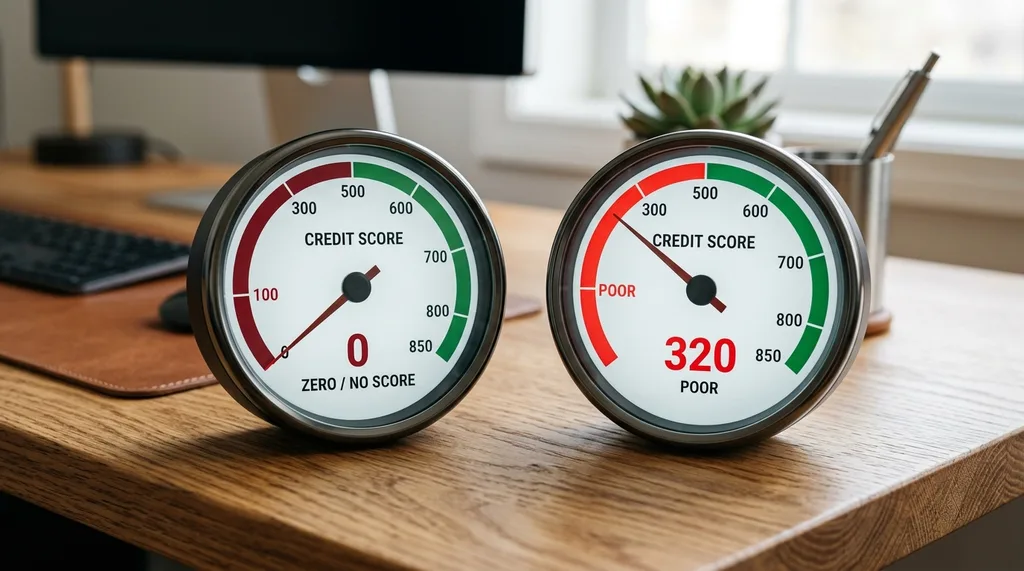

Having no credit does not mean you have a score of zero. It means scoring models like FICO and VantageScore cannot generate a score for you because there is no data to calculate one from. You exist outside the credit system entirely.

What does bad credit mean?

Bad credit means your credit report contains negative marks that pull your score down. Under the FICO credit score ranges, a score between 300 and 579 qualifies as poor. VantageScore classifies scores between 300 and 499 as very poor and 500 to 600 as poor.

Common causes of bad credit include late or missed payments, maxing out credit cards (using more than 30% of your available limit), defaulting on loans, and legal records like bankruptcies or foreclosures. Identity theft and fraud can also damage your score without any fault of your own.

No credit vs bad credit: a side-by-side comparison

| Factor | No Credit | Bad Credit |

|---|---|---|

| Credit report status | Empty or nonexistent | Contains negative marks |

| How lenders view you | Unknown risk | Known high risk |

| Time to improve | 6 to 12 months | 2 to 7 years depending on severity |

| Loan approval difficulty | Moderate (limited options) | High (higher rates, more rejections) |

| Interest rates offered | Higher than average | Highest available or denied outright |

| Best first step | Secured credit card or credit-builder loan | Pay down existing debt, dispute errors |

How no credit affects your life

Without a credit history, lenders cannot assess your risk as a borrower. Most will either reject your application or require extra security like a co-signer or collateral. This affects more than just loans. Landlords often run credit checks before approving rental applications, and some employers review credit reports during the hiring process.

The upside is that no credit is a clean slate. You have no negative marks to overcome, and you can start building a positive history from day one. The timeline to reach a “good” credit score from scratch is typically 6 to 12 months of responsible credit use.

How bad credit affects your life

Bad credit creates a cycle that is hard to break. Lenders either deny your applications or charge significantly higher interest rates to compensate for the risk. A borrower with a 580 FICO score can pay tens of thousands of dollars more in interest over the life of a mortgage compared to someone with a 740 score.

Bad credit also affects renting, employment, and insurance premiums in some states. If you are already dealing with a low score and need funds, understanding how to get a personal loan with bad credit can help you find realistic options.

How to build credit from scratch

Get a secured credit card

A secured credit card requires a cash deposit (usually 200 to 500 dollars) that serves as your credit limit. Use the card for small purchases each month and pay the balance in full by the due date. Most issuers report to all three bureaus, so your on-time payments start building your credit file immediately.

Become an authorized user

Ask a family member or trusted person with good credit to add you as an authorized user on their card. Their positive payment history gets added to your credit report, giving your score a boost without requiring you to apply for credit on your own.

Use credit-builder loans

Some banks and credit unions offer credit-builder loans specifically designed for people with no credit. The lender holds the loan amount in a savings account while you make monthly payments. Once you pay it off, you receive the funds and have a track record of on-time payments on your report.

How to repair bad credit

Pay every bill on time

Payment history accounts for 35% of your FICO score, making it the single most important factor. Set up automatic payments or calendar reminders to ensure you never miss a due date. Even one 30-day late payment can drop your score by 60 to 100 points.

Reduce your credit utilization

Keep your credit card balances below 30% of your total available credit. Below 10% is even better. Paying down existing balances is one of the fastest ways to see a score improvement, often within one to two billing cycles.

Dispute errors on your report

Check your credit reports from all three bureaus for inaccuracies. Incorrect late payments, accounts that are not yours, and outdated negative marks can all be disputed. The bureaus are legally required to investigate disputes within 30 days.

Apply for a card designed for bad credit

Several credit cards are specifically designed for people rebuilding their credit. These cards typically have lower limits and higher interest rates, but they report to all three bureaus. Use one responsibly for 6 to 12 months and your score will start climbing. Once your finances are more stable, you might explore online investment platforms to put your money to work.

Frequently asked questions

What is the main difference between no credit and bad credit?

No credit (credit invisibility) means lenders have no borrowing history to review. Bad credit means your history includes negative marks like late payments, defaults, or bankruptcies.

Is no credit better than bad credit?

Generally yes. No credit is a blank slate that you can build up in as little as six months. Bad credit carries negative marks that can take years to repair.

Can I get a loan with no credit score?

Yes, but options are more limited. Lenders may require collateral, a co-signer, or proof of steady income and employment to offset the missing credit history.

What are the most common causes of bad credit?

The most common causes are missed or late payments, high credit utilization (using more than 30% of your limit), and legal records like bankruptcies or foreclosures.

How do I build credit from scratch?

Start with a secured credit card backed by a deposit, become an authorized user on someone else’s account, or take out a small credit-builder loan. Pay on time every month.

Pingback: Free Legal Advice: How to Get Help Without Paying

Pingback: How to Secure the Perfect Home Loan: A Complete Guide